[ad_1]

The lockdowns of 2020 may possibly have prompted shoppers to put a lot more revenue towards their environment, boosting revenue for property enhancement suppliers Lowe’s (NYSE:Low) and House Depot (NYSE:High definition), but the financial and housing availability crunches of 2022 are holding them there.

Home furnishings, electronics and residence workplace set-ups aimed at creating home a better put to are living and function fueled 2020 obtaining, but with shoppers going through increasing expenses of gas and meals, theyre going to home improvement stores to tackle repairs themselves and begin gardens. This is preserving development at Lowe’s and Dwelling Depot sturdy, producing them both of those possibly rewarding portfolio additions this summer months, in my impression.

Both of those possibilities have rising dividend yields, building them desirable for value buyers hunting to make passive cash flow as properly. Ahead of you add either of these household enhancement shares to your portfolio, although, there are some cons to consider.

Lowes

Lowes (NYSE:Low) is a residence advancement retail chain running in the U.S., Canada and Mexico. It delivers goods for construction, maintenance, repairs and reworking. The housing sector may well be cooling a little from the highs of 2021, which may well inspire jobs in the home youre in.

Revenues for the organization have doubled around the earlier ten years, and earnings for every share are predicted to improve all-around 13%. Lowe’s has a dividend yield of 1.66%, and the firm has a extended observe file of increasing dividends. That could assistance sweeten the offer for investors.

Analysts rate Lowe’s a obtain, even although bulls assume the enterprise faces threats from climbing curiosity prices, supply chain difficulties and flattening housing prices. Its truly worth noting that the median age of properties in the U.S. is 39 many years, an age when homes will have to have an rising amount of money of maintenance and could be candidates for remodeling.

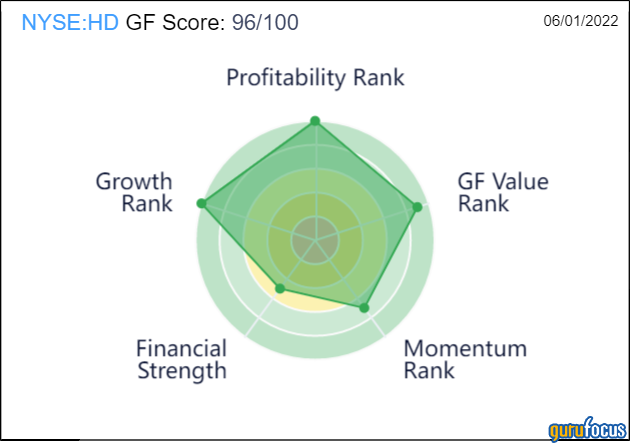

Lowe’s receives a GF Score of 96, pushed mostly by top rankings for profiability and advancement.

Residence Depot

Surpassing forecasts in nine of the very last 10 quarters, one more big U.S. property improvement retailer, House Depot (NYSE:High definition), just lately claimed 10.7% expansion in net income yr-more than-12 months.

Home Depot counts professional contractors between its largest buyers, and their huge-ticket purchases ended up up 18% throughout the past 12 months. EPS has grown 17% more than the previous three yrs and earnings is up 8% in excess of the earlier year, having it a obtain ranking from analysts.

Home Depot has a dividend yield of 2.26%, making it the much more attractive of these two shares for those in lookup of dividends.

Like Lowe’s, Property Depot also has a GF Rating of of 96/100. In addition to high expansion and profitability, it scores much better than Lowe’s for GF Price, even though it loses details for weaker momentum.

This write-up first appeared on GuruFocus.

[ad_2]

Supply connection

More Stories

How to Find a Local Electrician

Show Your Personality With An Ideal Bedroom

How To Choose The Right Concrete Floor Cutting Company